Vanguard to build a 12-inch fab in Singapore

TI should slow down its capacity expansion, but mature node pricing might hold up better than expected

Vanguard International Semiconductor (VIS) to build a 12-inch fab

Last week, Vanguard International Semiconductor (VIS) announced that they will build a 12-inch fab in Singapore through VisionPower Semiconductor Manufacturing Company (a JV 60% owned by Vanguard and 40% owned by NXP). Construction will begin at the end of this year with mass production to begin in 2027. Total investment will be USD 7.8 billion (USD 6.8 billion is for capex and USD 1 billion for working capacity, technology license fee). The target process node will be 130-40nm.

Who is VIS?

VIS started out as a producer of DRAM in 1994 before it transitioned to a logic foundry in 1999 with the support of TSMC. By 2004, the DRAM business was terminated, and it became a pure-play logic foundry. It made 3 acquisitions in 2008, 2014 and 2020 which were great deals on hindsight.

VIS has been an associate of TSMC as the latter owns 28% of VIS. In the early years, TSMC did the technology transfer and refer customers to VIS. TSMC is now a much lower percentage of VIS’s overall revenue. TSMC will be assisting VIS again by licensing the technology for 12-inch to VIS for less than US$1 billion. This is a very good deal for VIS as the required R&D costs will have been higher.

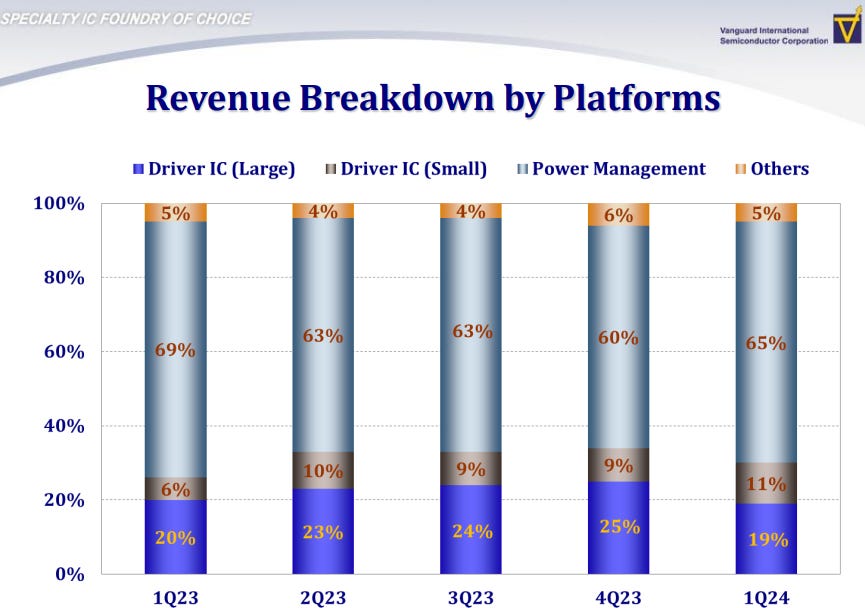

Power Management IC (PMIC) and Display Driver IC (DDIC) are the biggest revenue driver for VIS. DDIC has been on a decline and a huge part of which is referred by TSMC.

Source: Vanguard

Transition to 12-inch was inevitable

The 12-inch fab in Singapore is significant for VIS as it has been a pure play 8-inch foundry for the last 2 decades. Chinese competitor Hua Hong had expanded into 12-inch back in 2018. It was also getting costly to expand 8-inch capacity as the WFE companies no longer produce 8-inch equipment. Vanguard was able to repurpose DRAM fab from Winbond and Nanya Tech during past downcycles, but DRAM makers have been mostly profitable ever since they consolidated into a 3-players oligopoly. This resulted in an 8-inch shortage in 2017 that led customers to realise they might have to migrate to 12-inch eventually.

The writing was finally on the wall with the rise of Nexchip and the massive 12-inch capacity buildout by Texas Instrument (TI).

Nexchip is the 3rd largest foundry in China, established by Powerchip and Hefei government. Nexchip’s aggressive expansion and pricing have led to utilisation pressure for Taiwanese foundries such as Vanguard, PSMC and UMC. Nexchip is now the leading foundry for DDIC, a competitive component where cost advantage is important. In Q1 2024, Nexchip was able to maintain a utilization rate that is more than 20% higher than Vanguard and PSMC. Longer term, it is inevitable that Nexchip will gain market share in DDIC foundry.

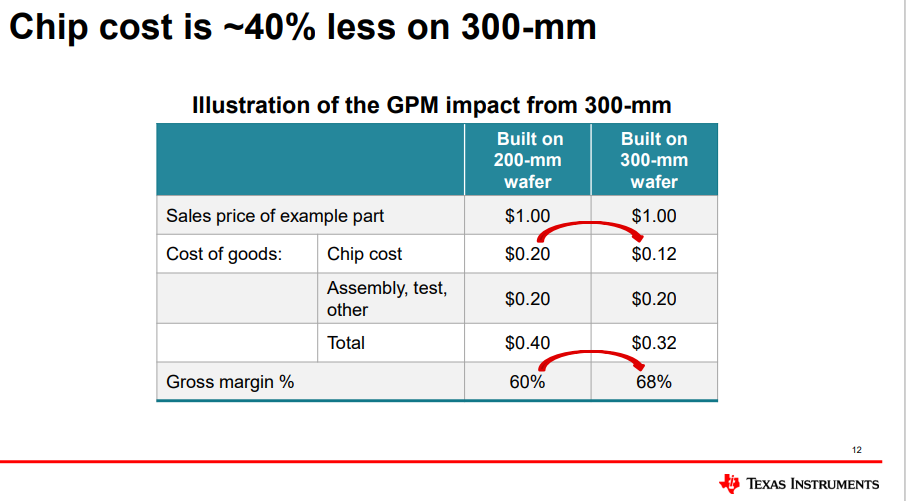

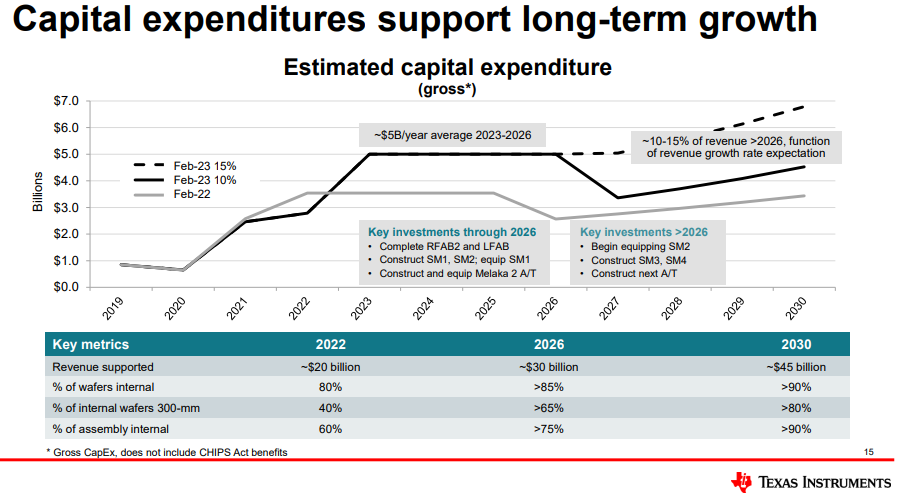

For years, Vanguard has been shifting its product mix away from DDIC to PMIC as PMIC has higher gross margin and better structural growth. However, TI started to promote the 40% cost advantage of using 12-inch wafer to produce PMIC. TI wanted to raise the proportion of internal 12-inch wafer production to 65% by 2026 and 80% by 2030. TI’s aggressive capacity expansion and migration to 12-inch created concerns for other PMIC companies who have been relying on 8-inch production. This was further exacerbated when TI started a price war in China last year. If demand growth is lesser than its capacity expansion, TI will have to cut price to fill its fab. Utilisation rate is a key driver of gross margin and cash flow for the company.

Source: Texas Instrument Capital Management 2023

Implication: Things might not be as bad for mature 12-inch

There are many mature 12-inch fabs ramping around in and outside of China.

Vanguard plans to ramp up to 55k wpm at its Singapore fab by 2029

PSMC plans to ramp up P5 fab in Tongluo to 45k wpm in 2027 and 100k wpm in 2030

PSMC is also working with Tata in India and SBI in Japan for greenfield projects

Nexchip will ramp up 30k wpm in its Fab 3 in 2024

Hua Hong’s 1st 12-inch fab is expected to reach the full designed capacity of 95k wpm in 2025. The 2nd 12-inch fab will ramp up to 83k wpm by 2027

Concerns about potential oversupply of mature 12-inch capacity exist, but it might be too premature to generalize the entire mature 12-inch as oversupply. Power Discrete and PMIC are 2 segments that have been transitioning from 8-inch to 12-inch due to competition. Power discrete might be oversupplied with the ramp of IDMs capacity in China, but the demand from pure fabless customer such as StarPower is strong too. In segment such as DDIC, the oversupply will hit harder as most of the applications are consumer related and cost will be a greater concern for customers.

For pricing, overseas capacity might not be as affected by the rapid growth of domestic China capacity. Customers are getting worried about geopolitics and the trade war between China and US. In sensitive areas such as AI, these chips are usually made outside of China. As customers are willing to pay a double-digit premium for capacity outside of China, overseas fabs are unlikely to be hit hard by the China capacity ramp. Chinese foundries are starting to see a rise in utilisation rate as the worst of inventory correction is over and Chinese fabless customers have shifted their foundry supplier mix. Pricing could even inflect upward if overall demand for smartphone, PC, industrial and automotive improve.

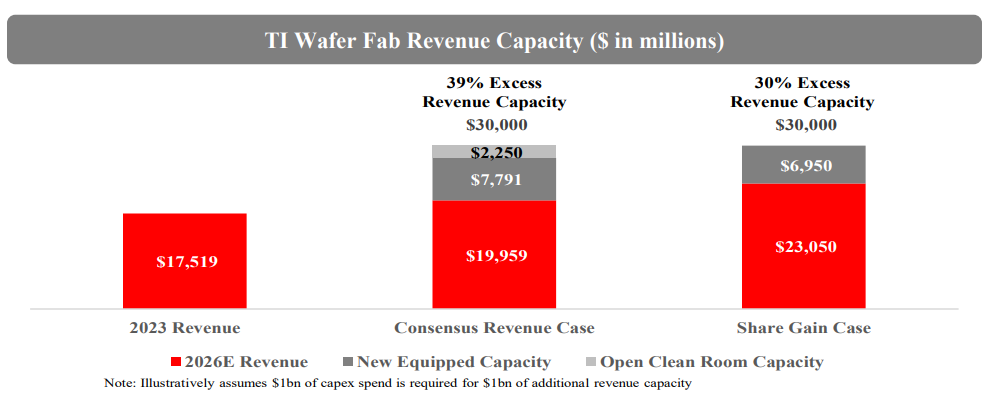

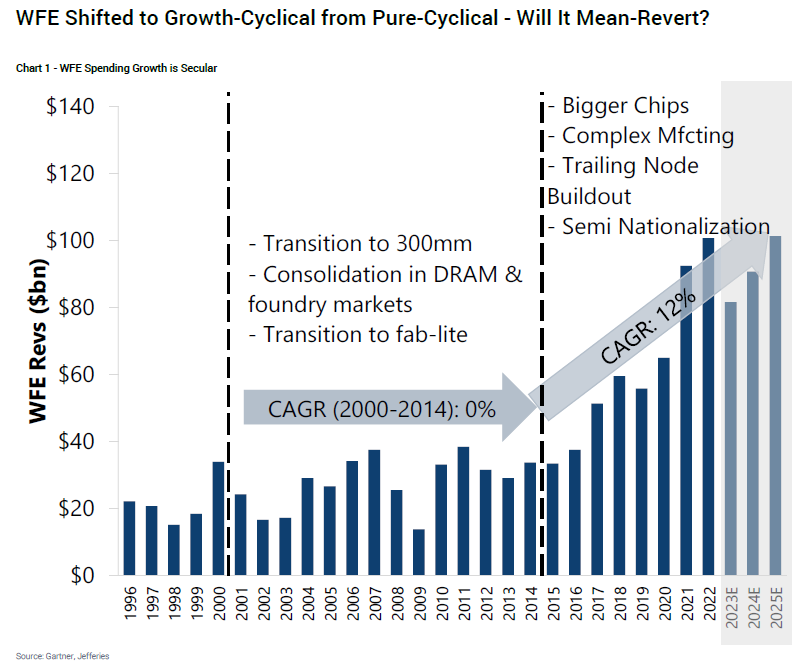

Back to Texas Instrument, the letter from Elliott may have prompted them to consider a reduction in their mid-term capacity expansion. Internal capacity is worth a premium only when there is a global shortage in capacities. This is unlikely to be a problem in the foreseeable future given the much higher WFE we have seen in recent years. The chip shortage in 2021 was a result of the underinvestment from 2008 to 2016 as the semiconductor industry rapidly consolidates. TI’s investment in 12-inch has also prompted their competitors to jump on the 12-inch capacity from the foundries. PMIC pricing will be under pressure as it used to before 2010. There is certainly room for TI to push out part of its capex since the expectation of EV penetration has been pushed out.

Source: Elliott

Source: Jefferies