Q1 Results: Qualcomm and Mediatek

Small unit shipment recovery and better mix to drive content growth

2024 smartphone market guidance

Mediatek is guiding for unit shipment to grow 2% to 1.2 billion units, but addressable market can grow low teens due to mix shift towards high-end smartphone

Qualcomm has guided for high single digit to low teens growth of 5G smartphones in 2024

The smartphone market reached a peak in 2017 and has been on a decline ever since. With a global smartphone population of 4.3 billion, the market is driven increasingly by replacement demand rather than new demand. There is hope that 1.1 to 1.2 billion could be the bottom for global smartphone shipments going forward. This is the 7th year since the peak of smartphone unit shipments in 2017. If we looked at the history of the PC market, PC shipments peaked in 2011 before bottoming 5 years later in 2016.

Source: Counterpoint Research

Source: Statista

For Q1, Mediatek’s mobile revenue grew 84% YoY as they benefitted from a low base and restocking demand. 2 quarters of restocking demand have ended and Mediatek is guiding for sequential decline (flat to high single digit) in Q2 and 2H revenue.

On the other hand, Qualcomm reported a better guidance with QCT revenue set to decline 2.5% sequentially on Apple and Samsung seasonality.

The mix shift is playing in the favor of Qualcomm who is the market leader in the high-end smartphone market. Qualcomm said that revenue from Chinese OEMs grew by more than 40% in 1H 2024, with strong demand for Snapdragon 8 Gen 3 in China. Samsung S24 has also performed above expectation with the debut of its AI smartphone.

In addition, Skyworks has also confirmed that it is losing more than 10% of RF content in the next generation of iPhone to Qualcomm. Qualcomm has seen a fair amount of success in its entry into the RF market through the bundling of RF and modem. This could reverse when Apple can come up with its own modem in 2026, but we have also seen that the timeline has been pushed back a few times.

Smartphone content growth

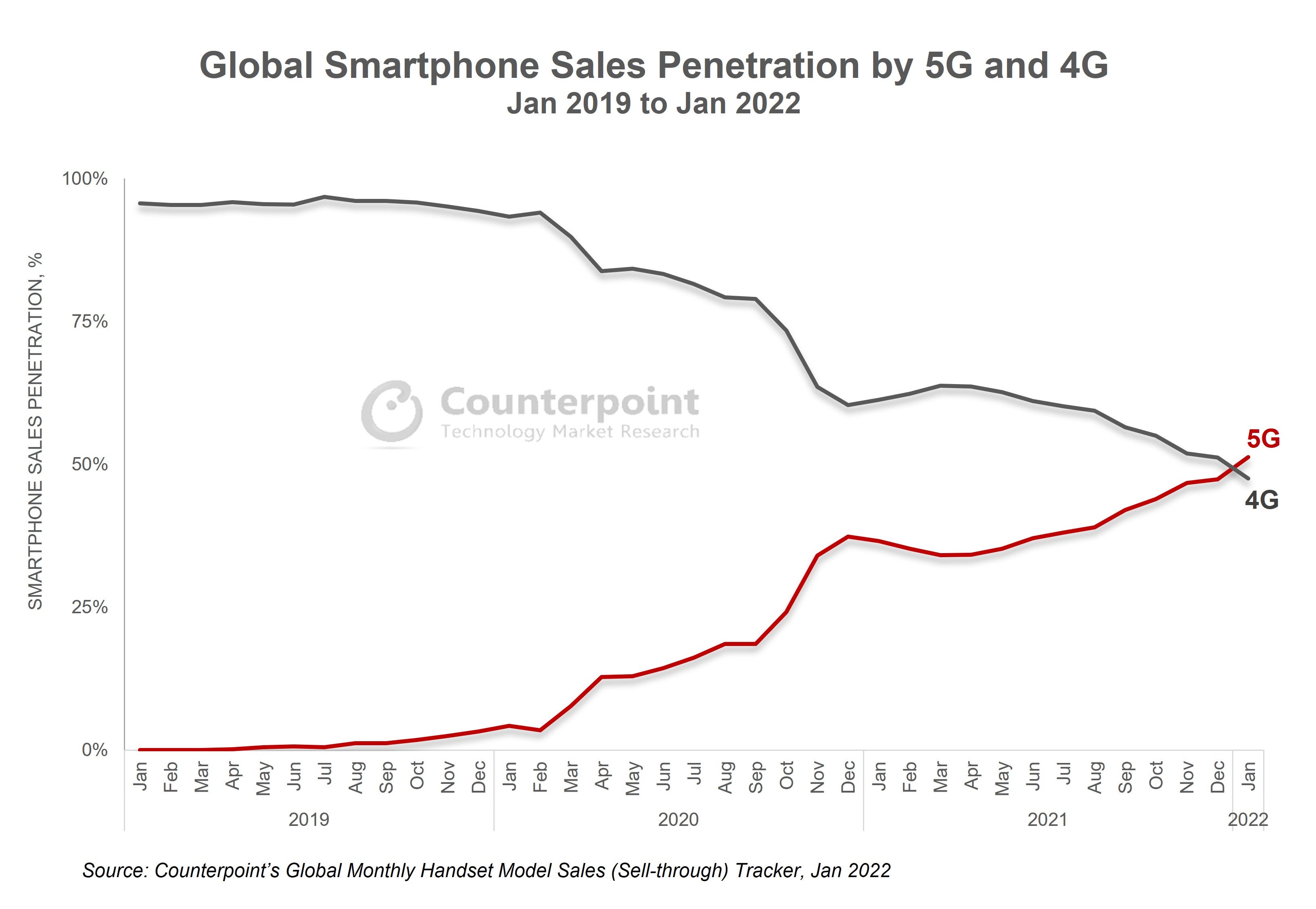

Despite the stable smartphone unit shipment, both Qualcomm and Mediatek can still benefit from content growth. After the launch of 5G smartphone in 2019, 5G penetration grew rapidly to 50% in 3 years. In the same period, Mediatek saw its mobile revenue grew by more than 3x from 2019 to 2022 despite a continuous decline in global smartphone shipment. Qualcomm’s QCT revenue grew by more than 2.5x in the same period. While the merchant silicon companies also benefitted from the demise of Huawei, the much higher pricing of 5G SoC had been a bigger driver of their revenue growth.

Source: Counterpoint

AI on the edge could be the next driver of semiconductor content growth in smartphone. Both Qualcomm Snapdragon 8 Gen 4 and Mediatek Dimensity 9400 will launch in 2H 2024 to address AI on the edge. In order to handle 7 billion parameters LLM, the NPU die size will be enlarged. Both chipsets will also be produced at TSMC N3. Bigger die size at more advanced node is good news for Mediatek, Qualcomm and TSMC.

Unlike AR/VR, penetration of AI smartphone will be driven by OEMs instead of consumers. Most high-end smartphone models should have AI capabilities in 2025 given the intensifying competition among the OEMs. Assuming 30% penetration rate and 10% bigger die size, this is still a good growth story for the next 2 years.

Beyond smartphone

Qualcomm has been actively diversifying into IOT and automotive for many years with its elevated R&D spending. Automotive is where Qualcomm has been successful especially in the area of infotainment. The company raised their total automotive design pipeline from $30 billion in September 2022 to $45 billion today. Current annual revenue run-rate of automotive is $2.4 billion or 6% of revenue and this is expected to grow to more than $4 billion by FY 2026. Despite the >30% CAGR until 2026, this will at best be 10% of Qualcomm revenue.

Qualcomm has also been working on ADAS and this has led to a partnership between Nvidia and Mediatek. Mediatek is expected to launch auto cockpit Dimensity product in 2026 after licensing IP from Nvidia. Revenue in the initial year is likely to be less than $1 billion for Mediatek.

Qualcomm will be launching Snapdragon X Elite in the middle of the year to target the AI PC market. Snapdragon X Elite will have first mover advantage, being the first to achieve 45 TOPs. However, both Intel and AMD will launch their AI PC CPU in 2H 2024. Mediatek has always been a market leader in supplying the Chromebook market. It will also start to supply Dimensity 9300 for Samsung’s high-end tablet at the end of the year.

For Mediatek, the design win for TPU is a bigger opportunity in 2026. Broadcom is certainly the leading player for Google’s TPU project with their strong SerDes IP. TPU has also been the most successful of the AI ASIC projects. However, with the high margin that Broadcom commands, Google will be carving out a part of the pie to Mediatek. Alchip is trying to get in, but there is limited incentive for Google to introduce another company right now.

Conclusion

With both companies trading at teens P/E and FCF multiples, they could do decently well with the launch of AI smartphones in 2H 2024. Mediatek has a dividend payout ratio of more than 80% after the end of NT 16 per share in special dividend this year. The dividend yield of Mediatek is around 6% and is much higher than the 2% for Qualcomm. Qualcomm’s share buyback has been unable to bring down total shares outstanding materially in the last few years due to the share-based compensation.