China is a bullish driver for global semiconductor demand

Memory strength, China is all-in AI

This was a busy week for me on Twitter as we are finally seeing the positive demand effect of DeepSeek.

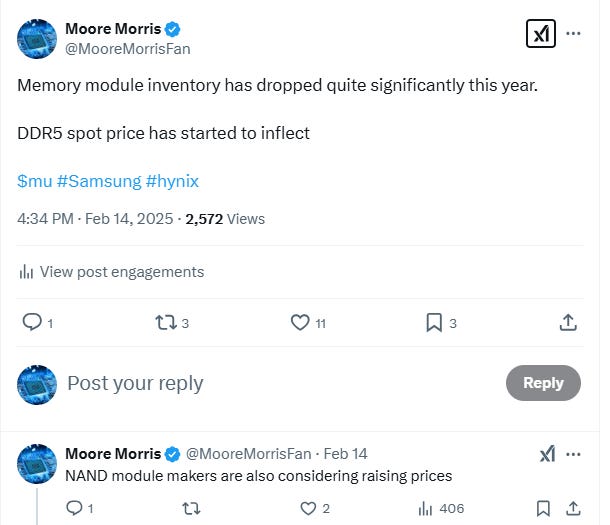

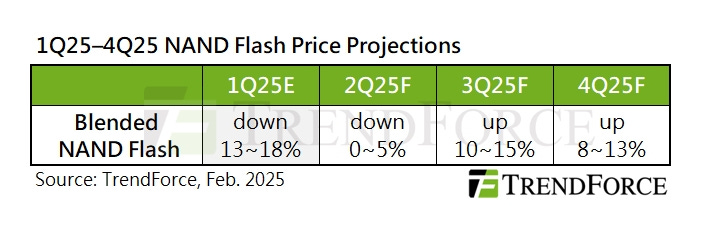

In memory, we are starting to see uptick in DDR5 prices while Trendforce is seeing NADN price inflection in 2H. China’s 3C stimulus (15% of smartphone ASP, capped at RMB 500) had led to a demand uptick in both PC and smartphone. In the 1st week of the government subsidies (Jan 20), smartphone sales in China grew by 60% yoy or more than 30% if adjusted for CNY. This led to a drawdown in memory inventory, reducing the temporary oversupply situation. NAND price is inflecting in 2H as multiple producers (Samsung, Micron, Hynix) have started to cut NAND production.

Memory demand is likely to further accelerate into 2H 2025. iPhone 17, which will be launched in Q3 2025, will feature an upgrade in DRAM memory content from 8GB to 12GB. According to TP Huang, most of the major smartphone OEMs will incorporate DeepSeek into smartphone. Running DeepSeek model could drive replacement demand and higher DRAM content for the inference.

China is all-in on AI

Despite the initial fear of DeepSeek on GPU demand, we have seen massive Jevons Paradox in play in China. The adoption of DeepSeek R1 throughout China is driving inference demand through the roof. Taiwan’s supply chain first heard the news of the increase in Hoppers orders right after CNY is over. In the middle of January, Hopper forecast was slashed by 80-90%. Last week, Hopper forecast has doubled from the January lows and this is certainly not the end.

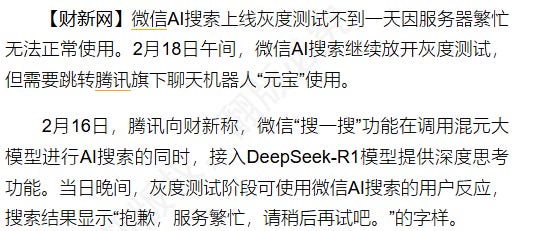

Tencent had ordered 200k H20 GPUs and a lot more is needed to serve R1 to more than 1.3 billion users on WeChat. On the 1st day of beta testing on WeChat, there was insufficient server capacity and Tencent had to subsequently redirect traffic to their chatbot YuanBao. Tencent will report results next month, so we will know the magnitude of increase in capex.

独家|微信AI搜索调用量超载 搜索需求跳转至聊天机器人“元宝”

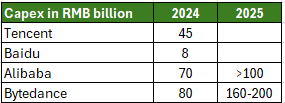

In the latest earnings, Alibaba said that the pursuit of AGI is their primary objective and that the investment over the next 3 years will be more than what they have invested in capex the last 10 years. This will work out to be at least USD 14 billion in capex this year and possibly even much higher in 2026. It is possible for Alibaba to spend as much as USD 25 billion in capex in 2026. Bytedance might also raise their capex to RMB 200 billion from the initial expectation of RMB 160 billion.

There will also be more capex from China Mobile, China Telecom and China Unicom. China SASAC (State-owned Assets Supervision and Administration Commission of the State Council) has issued a call for Central SOEs to study and implement the spirit of President Xi’s speech on developing AI. This is China all-in on AI, a national movement that is bigger than any sovereign AI effort we have seen.

In short, DeepSeek for China is the equivalent of ChatGPT moment in the USA. The massive increase in data center spendings the last 2 years by the FAMG will now be replicated in China. The difference this time is that the demand in China will be primarily driven by inference rather than training. Inference demand represents monetization opportunity and we will not doubt the capabilities of Chinese to integrate them in applications. Nvidia’s H20, RTX 5090 and RTX 4090 are highly sought after now. This demand will continue for as long as US government does not ban the chips.

At the same time, there will be a proliferation of domestic AI chips made by Chinese companies such as Huawei, Cambricon, Alibaba’s T-Head, Meta-X, Biren and e.t.c. Most of these will be manufactured at SMIC, whose capacity will now be the bottleneck for Chinese effort at domestic substitution for AI chipset.

Many listed Chinese companies will be a big beneficiary similar to their US and Taiwanese counterparts the last few years. Here is a list of companies in the Chinese supply chain:

Foundry: SMIC (981 HK)

Data Center: GDS, 21Vianet

GPU: Cambricon (688256 CN), Hygon (688041 CN)

Liquid Cooling: Shenzhen Envicool (002837 CN)

Networking Switch: Ruijie Network (301165 CN)

AI Chip Testing: Shanghai V-Test Semiconductor (688372 CN)

Optical Transceivers: Huagong Tech (000988 CN)

Server ODM: Inspur (000977 CN), Dawning Information (603019 CN)

Power Supply: Megmeet (002851 CN)