BYD Semiconductor Deep Dive

Unpacking the bear thesis on power semis and TSMC’s footnote in the story

Who is BYD?

BYD was founded in 1995 as a battery manufacturer and quickly became a global leader in the rechargeable battery market. The company entered the automotive industry in 2003 by acquiring Xi’an Qinchuan Automobile Company. Leveraging its strength in battery technology, BYD pivoted toward electric mobility, becoming one of the earliest Chinese producers of Electric Vehicle (EV or known as NEV in China).

When looking at power semiconductor, it is important to understand BYD as it is the largest EV producer globally. In 2024, BYD delivered 4.27 million electric vehicles (both battery electric vehicles [BEVs] and plug-in hybrid electric vehicles [PHEVs]), accounting for approximately 25% of global EV shipments. This figure is also 2.5 times more than Tesla’s 1.7 million units. China is the biggest EV market globally as it accounts for 65% (11.2 million units) of the global EV sales (17.1 million units).

BYD is bold in its EV strategy and is instrumental in shaping the direction of China’s NEV industry. In 2022, it became the first in China to go all-in on NEVs as it discontinue production of internal combustion engine vehicles (ICE). In 2025, it announced the adoption of advanced driver-assistance system (ADAS) for all its EVs.

BYD’s vertical integration is a major competitive advantage that underpins its leadership in the global EV market. Unlike most automakers, BYD produces nearly all critical components in-house: batteries, electric motors, semiconductors, vehicle platforms, and even the software that powers its cars. It owns BYD Electronics, which is a listed company that acts as a Tier 1 OEM for BYD. BYD is known to procure up to 70% of components from its in-house subsidiaries. This level of vertical integration is high than Tesla which still relies on external partners for batteries and semiconductor.

In addition to its scale, vertical integration allows BYD to become the lowest cost producer. The status of lowest cost producer is critical for BYD to offer the most competitive pricing in the world. It can also drive a faster innovation cycle as we have seen with Blade Battery and DM-i hybrid system.

Let’s take a closer look at BYD Semiconductor, one of BYD’s most important subsidiaries after its battery arm, FinDreams Battery.

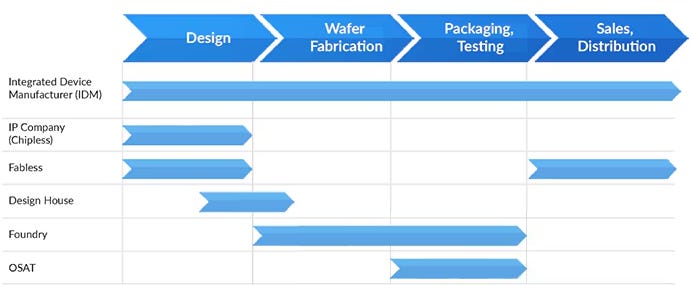

History of BYD Semiconductor

BYD Semiconductor was first established in 2002 as a fabless design company to research on battery protection IC. This was a year before it decided to went into the automotive sector in 2003. Subsequently, it also went into microelectronics, optics and LED.

In 2004, TSMC made the decision to shut down Fab 1. This was the company’s very first fab, originally located inside the Industrial Technology Research Institute (ITRI) where TSMC was founded in 1987. In 2005, all the equipment from TSMC’s Fab 1 was sold off as a complete line to establish a 6-inch fab at Ningbo SinoMOS Semiconductor (宁波中纬). Ningbo SinoMOS’s patents were mainly licensed from TSMC. Many of their engineers were also former TSMC employees, so there were some similarities in process technology and management.

Facing financial difficulties, BYD came in to acquire Ningbo SinoMos in 2008 for $29 million. They knew that IGBT will be a key component for electric vehicle. This is how BYD Semiconductor went from a fabless company to an integrated device manufacturer (IDM) that oversees the entire production process from design to manufacturing. In fact, BYD is also a system company that incorporates the chip made from BYD Semiconductor in its EVs.

Source: Samsung

BYD Semiconductor Portfolio

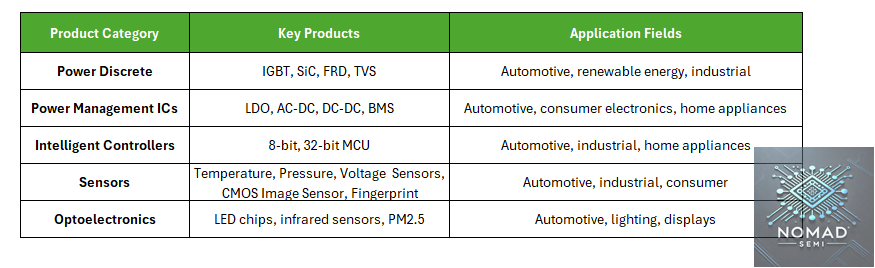

With more than 20 years of history, BYD Semiconductor has a wide product portfolio that can be broadly categorized as Power, MCU, Sensor and Optoelectronics. This can cover most of the semiconductor requirement in an EV other than infotainment SoCs and autonomous driving processors. While BYD Semiconductor has centered its strategy around automotive application, its products are also used in industrial, home appliances, consumer electronics and renewables.

Source: BYD Semiconductor

These are the known subsidiaries of BYD Semiconductor

BYD Ningbo Semiconductor

Based in Ningbo

The foundry that BYD Semiconductor acquired in 2008. Original equipment and process was from TSMC

First production base for IGBT 4.0

BYD Changsha Semiconductor

8-inch plant that started mass production in 2022

Annual capacity is able to fulfil the chips requirement for 500,000 cars

BYD Xi’An Semiconductor

Based in Xi’An, which is also BYD’s largest EV production base

R&D Center and the production base for IGBT 6.0

BYD Yangzhou Semiconductor

Based in Yangzhou, Jiangsu

Production site for DM-i 4.0 IGBT module

BYD Chengdu Semiconductor

Started construction in 2022

12-inch IGBT fab

BYD Shaoxing Semiconductor

Started production in 2023

Production of Power and optoelectronics

BYD Jinan Energen Semiconductor

Based in Jinan, Shandong

Producer of 8-inch silicon and silicon carbide (SiC)

Acquired in 2021 with Jinan government owning a minority stake. Foxconn was a former investor when it was founded in 2018

Guangdong BYD JieNeng

Based in Huizhou

Focus on optoelectronic semiconductor products such as LED lighting, optoelectronic modules and smart security

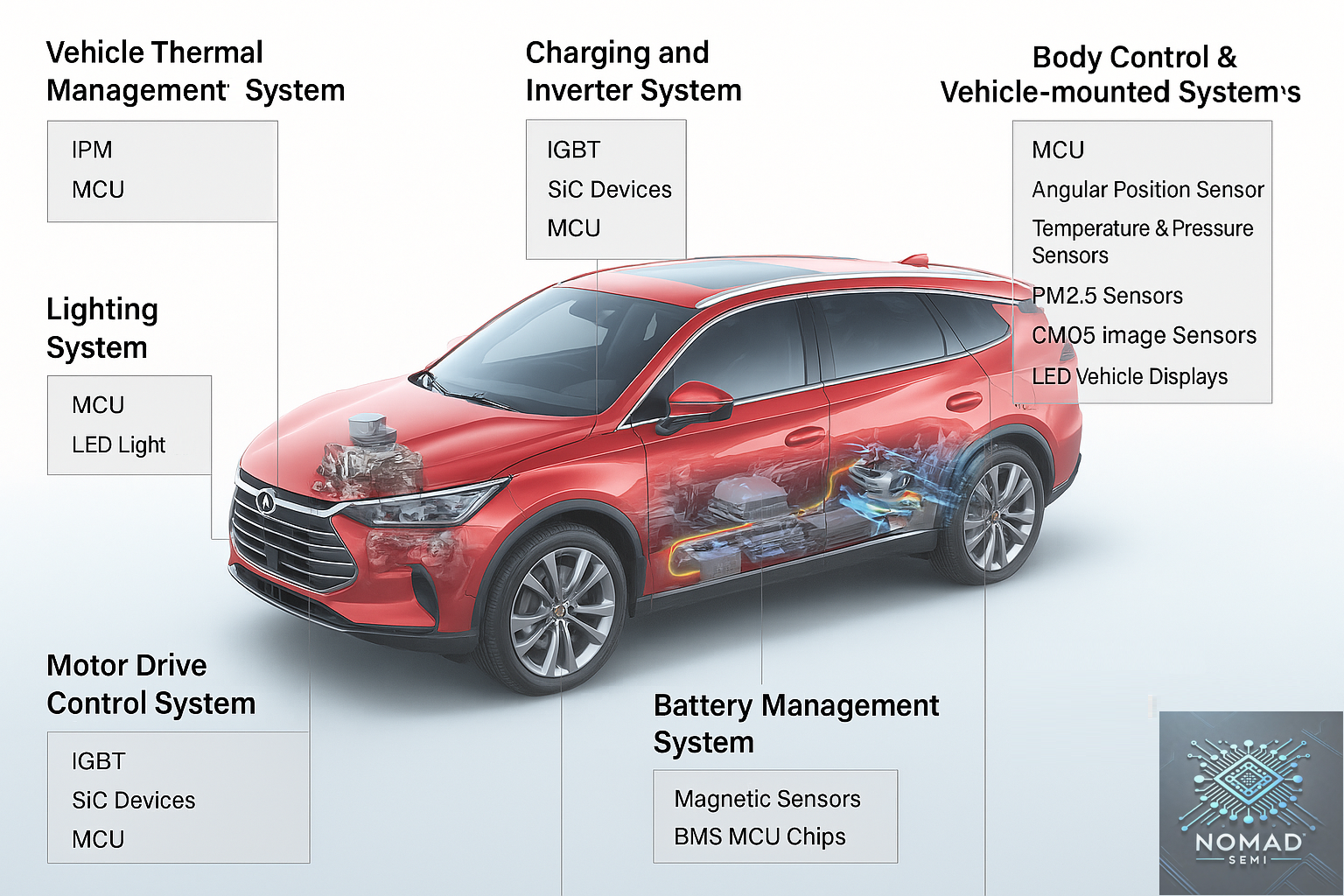

Power Discrete and Module

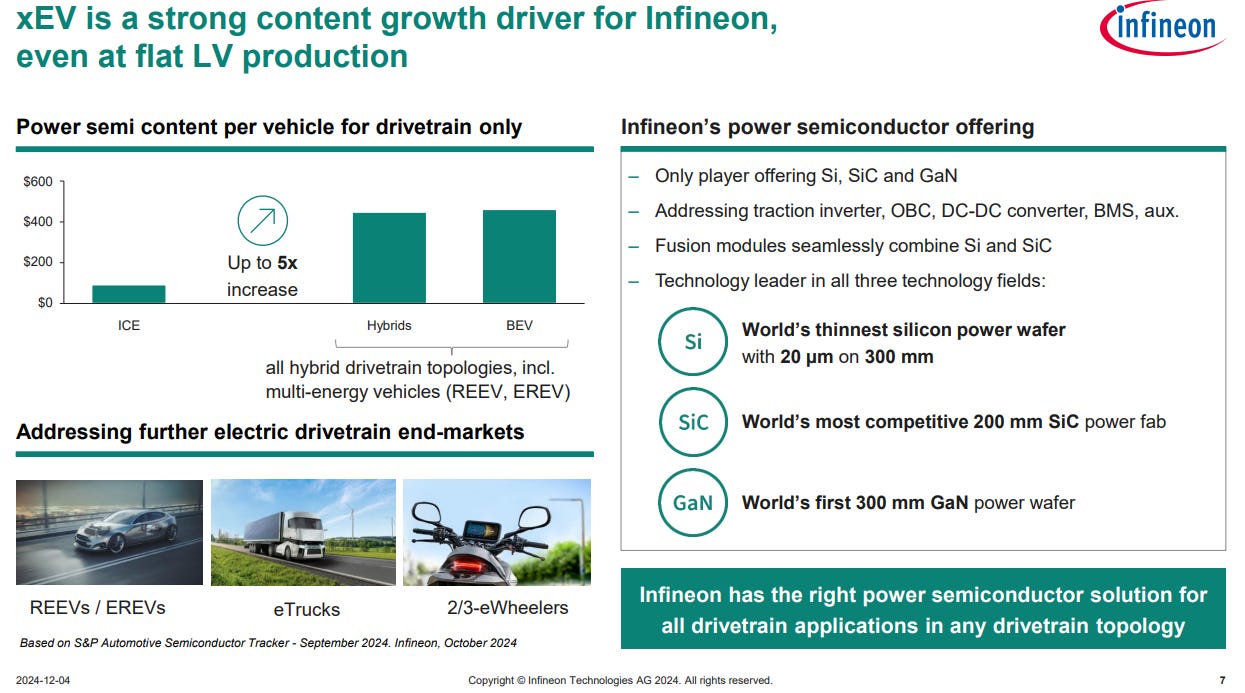

Of all the major product categories, Power Discrete is the most important for BYD both strategically and financially. Many of BYD’s innovations in its EVs would not have been possible without the support of BYD Semiconductor as the power semi content in EV is up to 5x higher than ICE. Products in this segment includes IGBT chips/modules, IPM modules, FRD chips, and SiC devices.

Source: Infineon

Fast Recovery Diode (FRD) is a semiconductor component designed to rapidly switch off after conducting current in order to minimize power loss and heat generation. Unlike standard diodes, FRDs have a much shorter reverse recovery time, making them ideal for high-speed switching applications such as inverters and motor drives. FRD is important in automotive where energy efficiency and thermal management are critical. BYD Semiconductor FRD chips can cover a voltage range of 650V to 1200V.

Insulated Gate Bipolar Transistor (IGBT) is commonly used in power electronics for switching and amplifying electrical signals. It combines the high efficiency and fast switching capabilities of a MOSFET with the high current and low saturation voltage handling of a bipolar transistor. This makes IGBT ideal for medium- to high-voltage applications such as inverters, EV motor drives and renewable energy systems.

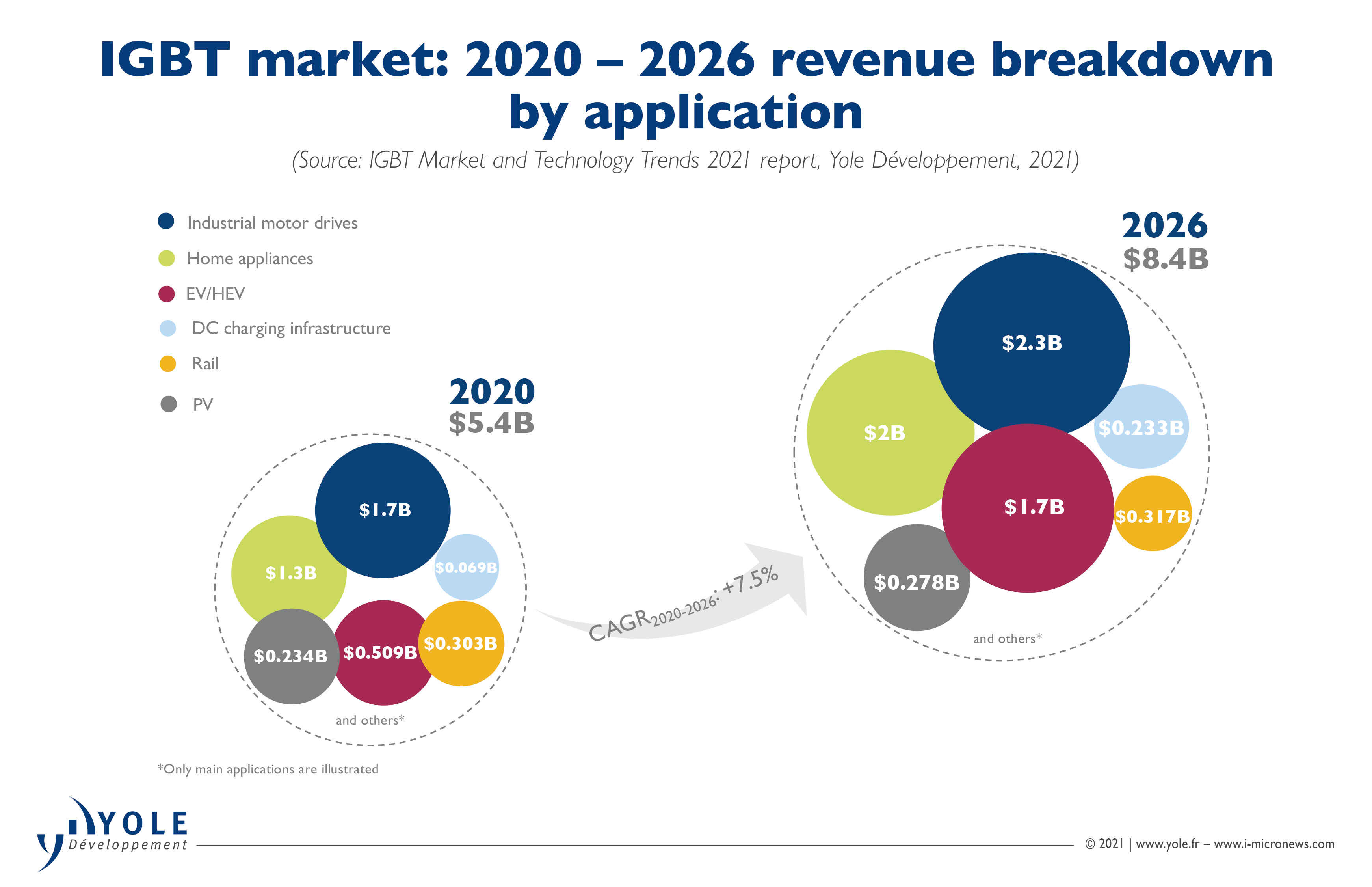

EV is driving strong demand growth for IGBT as every EV requires multiple IGBT modules for motor inverters, on-board chargers, etc. IGBT is crucial in EV powertrains to efficiently convert DC power from batteries into AC power to drive electric motors.

Source: Yole

BYD Semiconductor formed a team to do R&D on IGBT back in 2005. The first IGBT 1.0 chip was launched in 2009, followed by the IGBT 2.0 chip in 2012 and the IGBT 4.0 chip in 2018. Although it still lags behind international peers, the IGBT 4.0 chip incorporates a planar gate design that reduces overall power losses by approximately 20% and increased temperature cycle life by more than 10 times. In 2020, the IGBT 5.0 chip was produced based on the high density Trench FS technology. IGBT 6.0 chip was released in 2022 and BYD Semiconductor is no longer that far away in technology from the likes of Infineon. Today, BYD Semiconductor is the largest domestic supplier of IGBT for automotive in China.

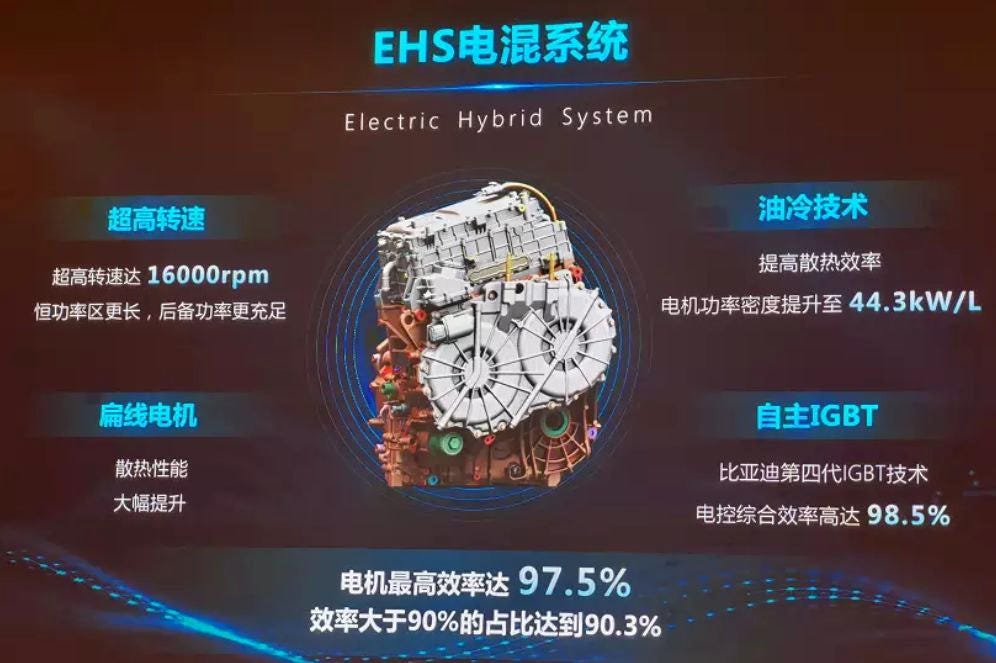

One of the key reason for BYD’s share gain in the recent years was the launch of the Dual-Mode Intelligence (DM-i) solution for its PHEV. DM-i 4.0 was first introduced in 2021 with a fuel efficiency of 3.8L/100km and cost parity with ICE. Unlike other hybrid system, DM-i will prioritize the use of electrical power which reduces fuel consumption. One of the core components of the DM-i 4.0 system is the Electric Hybrid System (EHS), which incorporates BYD's in-house IGBT 4.0 chip, enabling the electric control system to achieve an efficiency of up to 98.5%. The DM-i 4.0 IGBT module integrates the power drive, generation and buck/boost units into a single package, optimizing structural layout for a high degree of integration. This exemplifies how vertical integration and close collaboration with BYD Semiconductor enable BYD to achieve breakthroughs in its EV technology. Cost savings were also achieved through vertical integration, as the IGBT represents a significant portion of the EHS's overall cost. In 2024, DM-i 5.0 was introduced which reduced fuel consumption by 25% to 2.9L/100km and improved the range by 50% to 2100km.

Source: BYD

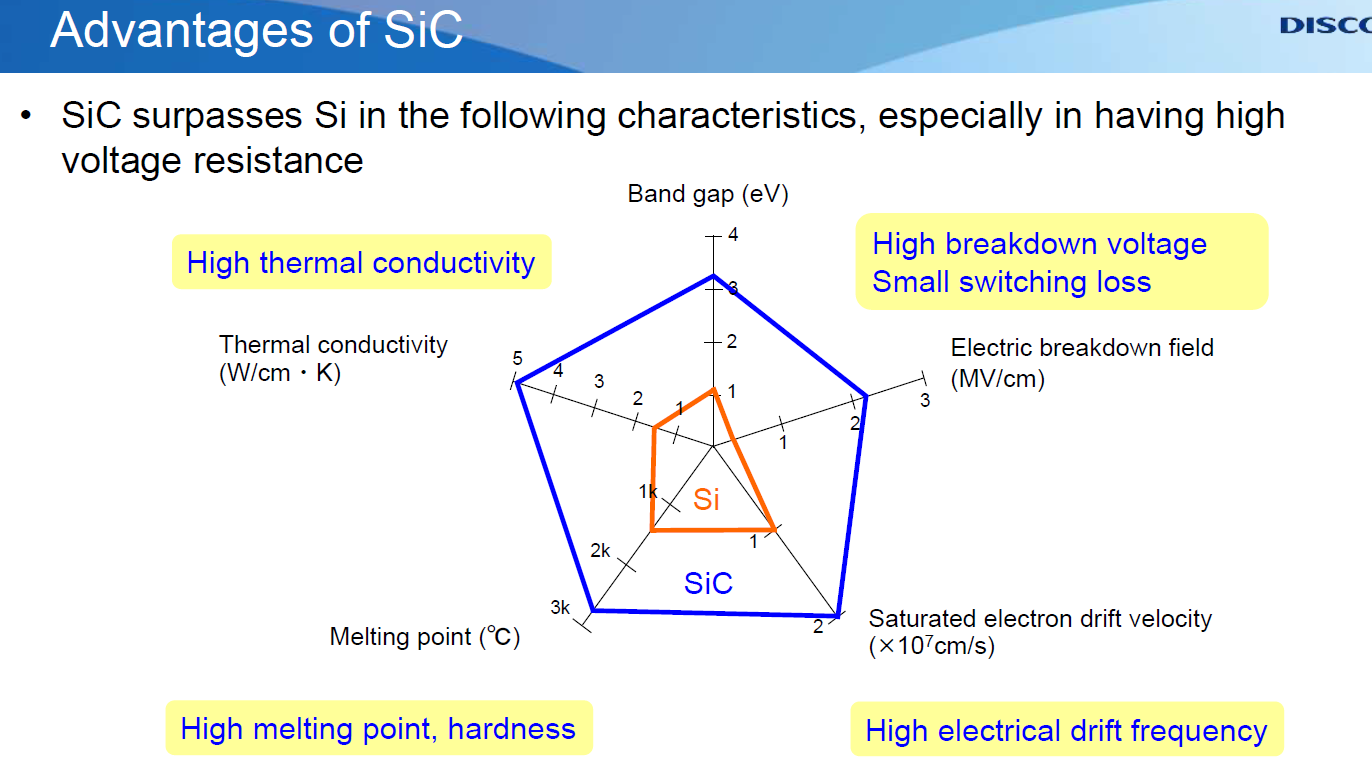

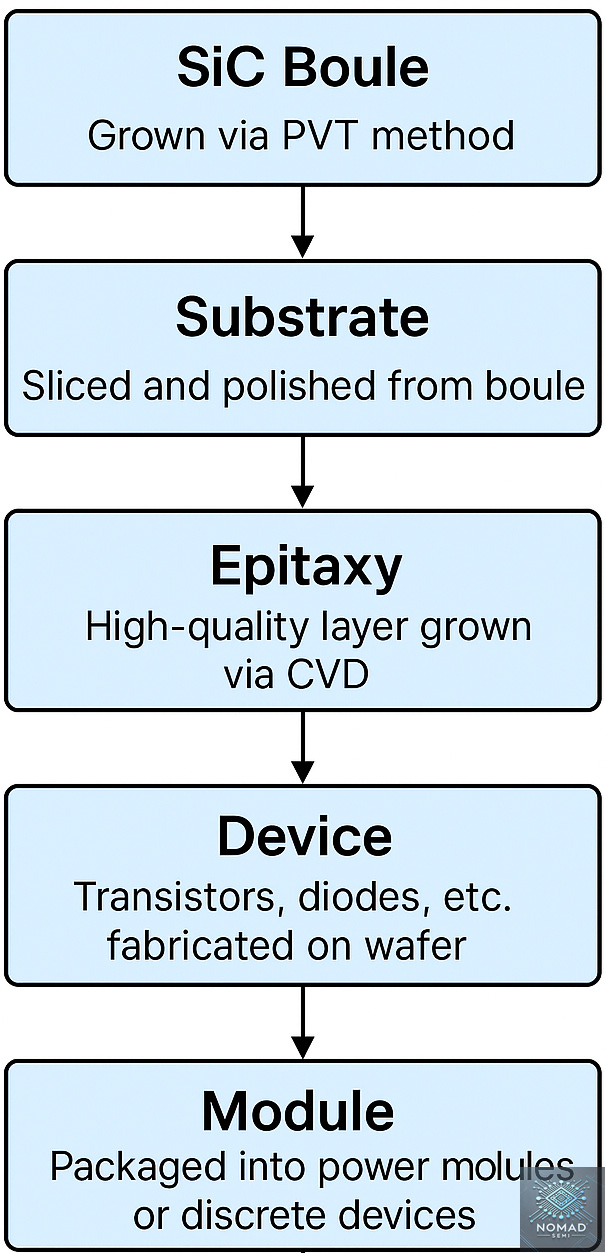

Silicon Carbide (SiC) is a wide bandgap semiconductor material that offers superior efficiency, higher thermal conductivity, and faster switching capabilities compared to traditional silicon. In EV, SiC is increasingly adopted for inverters, onboard chargers, and DC-DC converters where it enables more compact systems with reduced energy loss. Its ability to operate at higher voltages and temperatures makes it ideal for improving the overall efficiency and driving range of EVs, while also contributing to faster charging and better performance.

Source: DISCO

The main setback for SiC adoption is that it is much more expensive than traditional silicon. This is due to the complex and costly manufacturing process, which involves growing high quality SiC crystals. SiC is grown using a method called sublimation, which is more complex than the Czochralski method used for silicon wafer. As wafer size increases from 6-inch to 8-inch, maintaining crystal uniformity and minimizing defects across a larger area becomes much harder.

Additionally, SiC wafers are harder (Mohs hardness of 9.5 compared to 7 for Silicon) and more brittle, making them more difficult to process and resulting in lower yield. Wolfspeed has faced lots of difficulty in ramping its 8-inch Mohawk fab.

BYD Semiconductor had invested in SiC research for years and first introduced their three-phase full-bridge 1200V 840A SiC module for motor drives in 2020. In 2022, they released a 1200V 1040A SiC module that boosted power by 30% for their 800V platform.

1200V SiC HPD module, Source: CNEVPost

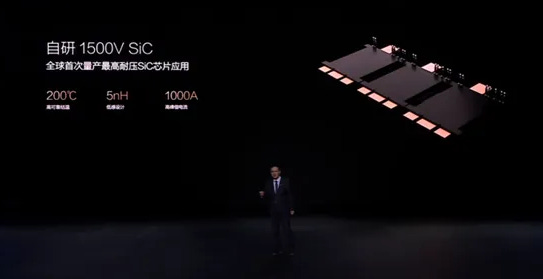

On March 17, 2025, BYD launched its groundbreaking Super E Platform, marking a significant leap forward in EV charging technology. The platform introduces a 1000V architecture and supports a peak charging power of 1 MW. With this advancement, BYD enables a fast charging rate of up to 10C (fully charging a 100 kWh battery in 6 minutes), compared to the current industry level of 6C. With its ultra-fast charging, Super E Platform vehicles can reach 2 km of range per second, or up to 400 km of range in just 5 minutes.

Source: BYD

This achievement was made possible by BYD Semiconductor breakthrough in high-power 1,500V SiC chips. It marks the first large-scale application of 1500V SiC chips in the global automotive industry. Through the use of laser welding technology, parasitic inductance has been reduced to 5 nH, and current capacity increased to 1000A. At the module level, it has shifted from the traditional HPD module to a half-bridge DCM architecture (compare the 1500V module below with the 1200V HPD module earlier). Double sided silver sintering is also used to enhance the thermal (Up to 200°C) and electrical performance.

Source: BYD

According to tphuang (very good source for BYD), BYD Semiconductor is working on 1700V SiC module which will enable >1000V platform. 1 advantage of BYD Semiconductor in China is that it is vertically integrated across the supply chain from the epitaxy growth to the final module. Unlike global players, Chinese companies are mostly involved in only 1 to 3 steps of the SiC manufacturing process.

Source: Knowmade

Smart Control IC

The core products under the Smart Control IC segment are MCU and PMIC.

Microcontroller Unit (MCU) is an integrated circuit that contains a processor core, memory, and input/output peripherals on a single chip. In a way, it is a simpler form of CPU that acts as the "brain" for controlling specific functions within electronic systems.

In the automotive industry, the use of MCUs is rapidly increasing due to the growing complexity and rising penetration rate of EV. From basic body control modules (like windows, lights, and wipers) to advanced driver-assistance system (ADAS), battery management system (BMS), motor control, and OTA updates, MCUs are essential for EV and intelligent cars.

BYD Semiconductor started to offer industrial-grade MCU in 2009 that can integrate functions such as control, RFID, capacitive touch sensing, and LED driving. They are adopted in small appliances like microwave, induction cookers and smart door locks.

BYD Semiconductor then extended its business to automotive MCUs and launched the first generation of 8-bit automotive MCU in 2018, followed by 32-bit automotive MCU in 2019. 8-bit MCU is simpler, cheaper, and typically used in basic control tasks like window, lighting, and seat adjustment. In contrast, 32-bit MCU offers much higher performance and are used in complex systems such as engine control unit (ECU), ADAS and BMS in EV.

In EV, precise control is required for the charging / discharging behavior, thermal status, and cell balancing of the battery. This is done through the BMS that processes data collected (current, temperature) and calculates the State of Charge (SOC). BMS is also able to increase the lifespan of the battery and ensures its safety. Reliability is important and BYD Semiconductor has achieved AEC-Q100 Grade 0 (temperature tolerance of up to 150°C) for its MCU. In 2021, BYD Semiconductor has shipped out more than 10 million units of MCU.

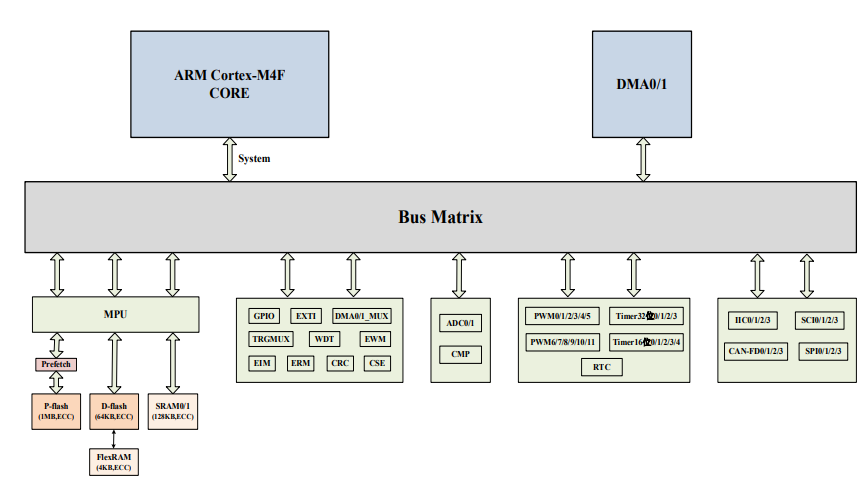

BS9046AM64 Block Diagram based on ARM Cortex-M4F core, Source: BYD

PMIC (Power Management Integrated Circuit) is a specialized chip that manages the distribution, conversion and sequencing of electrical power within electronic systems. In EV, PMICs play a critical role in ensuring efficient and stable power delivery across a wide range of subsystems with varying voltage and current requirements.

BYD Semiconductor started to supply battery protection IC for top-tier international phone brands as early as 2007. It also has AC-DC products that are primarily used in smartphone, laptop, networking device and smart home application. Most of the AC-DC converters are not automotive grade. For DC-DC converter, I can only find a single product BF1231. This is a relatively weaker product portfolio within BYD Semiconductor as compared to power discrete and MCU. Automotive is a relatively high-end product for TI and ADI.

Source: BYD

Sensors and Optoelectronics

BYD Semiconductor’s sensor line includes CMOS image sensors (CIS) for cameras (used in surround view systems, rear cameras and driver monitoring) and other sensors like magnetic position sensors (used in motors or pedals). The automotive CIS market is growing thanks to ADAS adoption as the number of cameras per car is increasing (rear camera mandated in many markets, plus front and side cameras for ADAS). BYD Semiconductor serves the automotive market with a range of CIS from VGA to 2MP, 3MP and 8MP. Current adoption rate is still mostly for driver monitoring in the car interiors. BYD Semiconductor also supplies low-end CIS for the smartphone and surveillance industry.

Source: BYD

Electromagnetic sensors convert physical quantities such as current, position, and pressure into standardized or application-specific electrical signals. They primarily include current sensors and angular position sensors. The company’s current sensors support a wide measurement range from 100A to 3,500A, while its angular position sensors achieve a detection accuracy of up to 0.05 degrees.

Optoelectronic Semiconductors includes LED lighting and display IC (LED drivers or small display ICs). This is a relatively mature market for BYD which allows BYD to cost down with BYD Semiconductor. Shaoxing plant is able to supply up to 6 billion optoelectronic units annually. Automotive LED products include Light Source, Smart Lighting, In-Vehicle Display and Intelligent Display.

One interesting product is the Far and Near Infrared Night Vision System, which offers advanced capabilities such as:

Pedestrian and vehicle detection and identification

Clear imaging at night, enabling visibility through darkness, glare, and haze

Glare suppression for oncoming vehicle headlights

This system significantly enhances driving safety and situational awareness, especially in low-visibility environments.

What else will they do in the future?

Recently, BYD founder Wang Chuanfu said that he would like to expand BYD Semiconductor from 5000 people to 8000 people.

It is also known that BYD is working on infotainment chip and ADAS chip in the future. Currently, BYD relies on Nvidia’s Orin, Black Sesame and Horizon Robotics for its ADAS solution. BYD ADAS chip is said to be able to achieve a performance of 80 TOPS which is still lower than its suppliers. Qualcomm is currently the market leader for infotainment chip in automotive.

Last year, BYD Semiconductor also said that they had open the world’s largest SiC fab that is 10x bigger than the 2nd largest SiC fab. That is a lot of capacity entering production!

Implication for Global Power Semiconductor

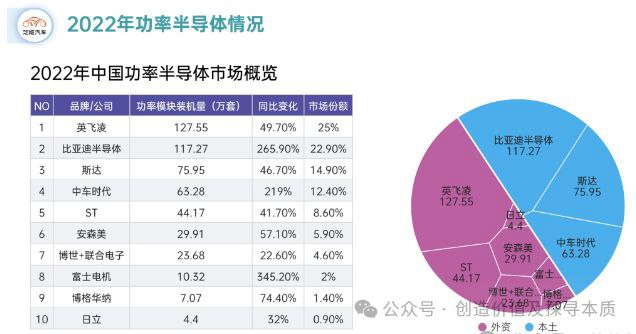

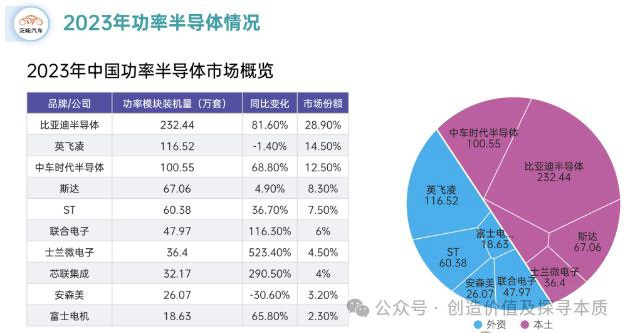

The rise of BYD and BYD Semiconductor is bad news for the global power semiconductor suppliers. Before I elaborate further, let’s look at the charts below. In 2022, Infineon (英飞凌) was the market leader for power module in China with a 25% market share. BYD Semiconductor (比亚迪半导体) was the No 2 in China with a market share of 22.9%. In 2023, BYD Semiconductor is now the market leader for power module in China with a market share of 28.9%, while Infineon has dropped to No 2 with a market share of 14.5% (-10.5% YoY). ST Micro and On Semi (安森美) also saw a reduction in their market share.

Source: WeChat

Source: Caixin

As we know by now, BYD Semiconductor can supply 70-90% of BYD’s IGT and SiC requirement. This ratio is the highest among all the global auto OEMs. If BYD gains share in the global automotive market, this is a share loss from the IDMs to the system company (An analogy will be ASIC consumed by hyperscaler vs merchant silicon purchased from Nvidia). The unfortunate news is that BYD is only going to gain market share in the global automotive and EV market.

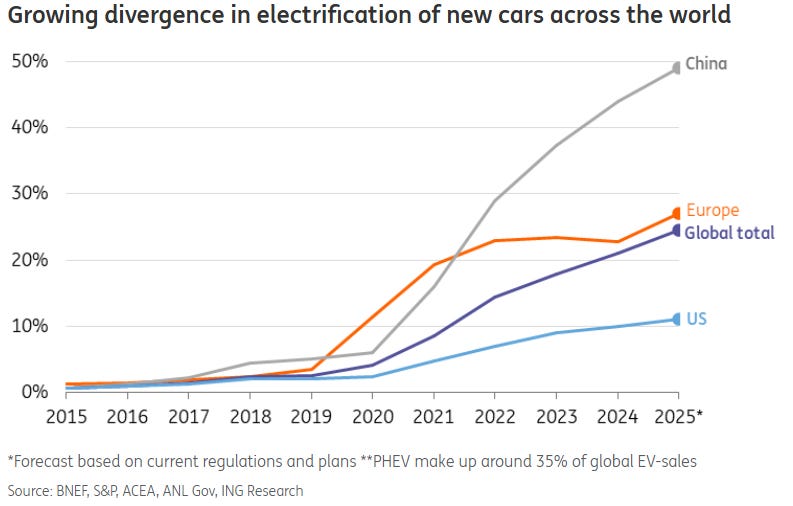

China has the highest EV penetration rate globally and is not showing any sign of slowdown. On the other hand, global EV penetration rate has slowed down with the Trump administration in US and the extension of EU CO2 emission target to 3 years.

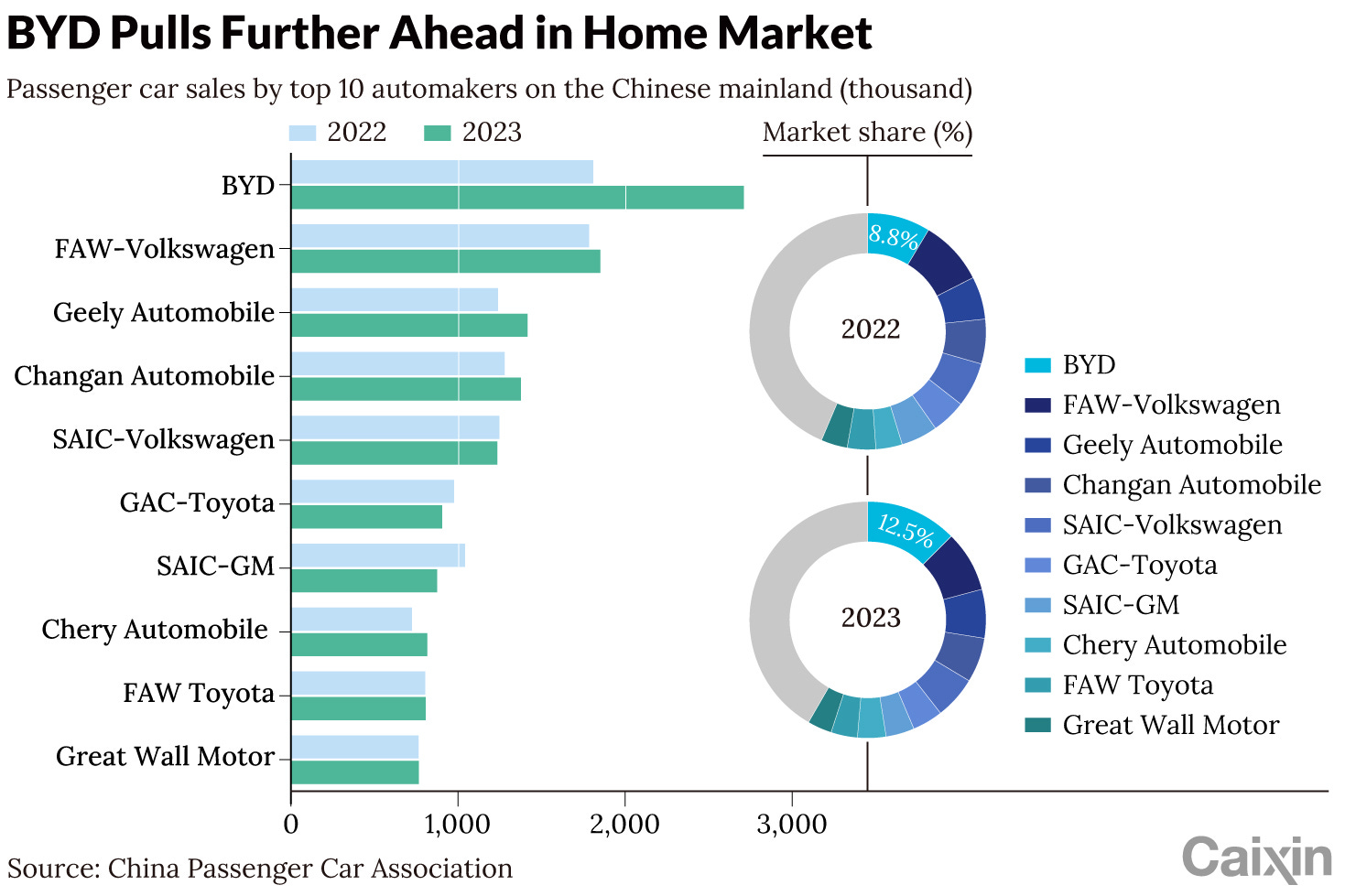

BYD’s market share in China will increase with the rising penetration rate of EV. BYD has 33% market share in China EV market and only 18% in China Passenger Vehicle market. EV penetration rate will be 60% in China in 2025 and BYD domestic sales is expected to increase by 20-30% this year.

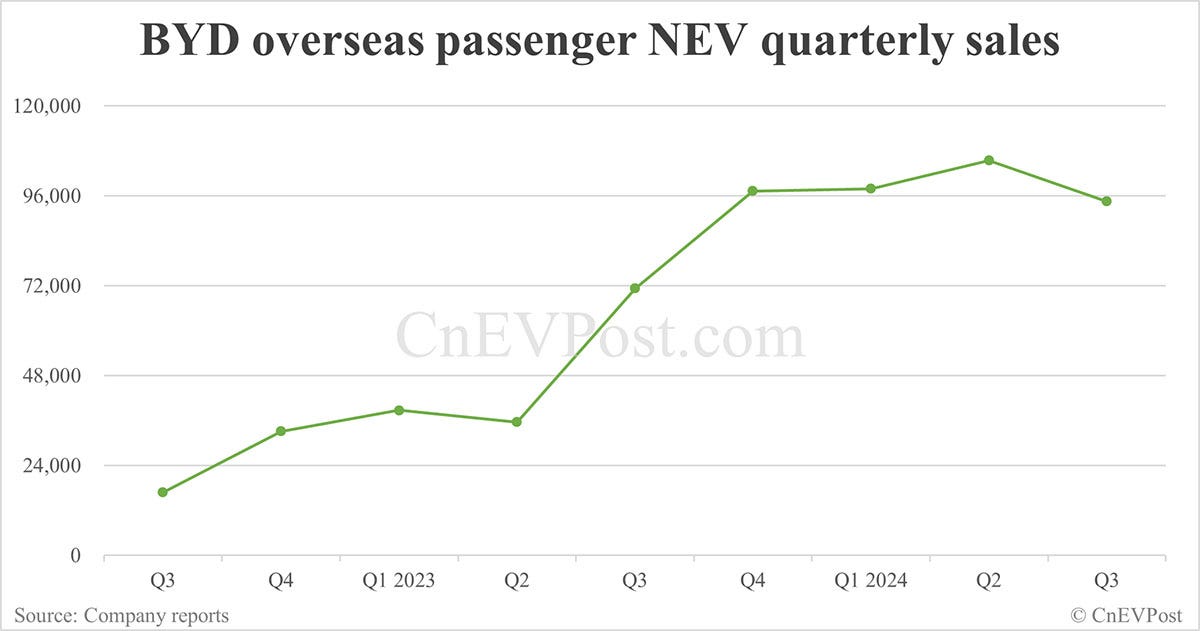

If you think that the threat is limited to China sales, BYD is growing its export market rapidly. Export sales took off in 2023 with 334% growth, followed by another 65% growth to 400,000 cars. BYD has guided for export sales to double in 2025 to 800k cars. BYD is doing very well in Asia, Latin America and Oceania due to its affordability.

Source: ING

Source: CnEVPost

Beyond BYD who is early to build their internal chip capability, other Chinese OEMs are also catching on to the strategic value of in-house semiconductor. Geely, the 2nd biggest NEV company in China, invested in Zhejiang Geener Microelectronics in 2022. Changan, the 3rd largest NEV company in China, formed a JV Chongqing Anda with StarPower. Great Wall Motor recently took over the full ownership of Wuxi Xindong. Li Auto is also known to be in the process of building an ADAS chipset with the support of Alchip.

Source: Gasgoo

Chinese EV companies are moving in the direction of system companies that control critical parts of the hardware stack from silicon to software. The rise of vertically integrated auto-chip players in China, with BYD Semi as the early incumbent and benchmark, will put pressure on all power IDMs.

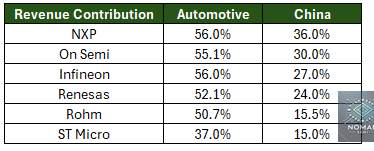

Among the global IDMs, we believe that NXP, On Semi and Infineon are most at risk from this rising trend of vertical integration within Chinese automakers. Automotive application is half of their sales for most of the global power IDMs. China revenue is also relatively high in contribution for NXP, On Semi, Infineon and Renesas.

Among the various chip verticals, we believe power discretes are most at risk, followed by MCUs. In contrast, barriers to entry remain higher for PMICs, CIS, infotainment, and ADAS. TI is also becoming vulnerable post the 125% tariff from China.

Another bear thesis for global power semiconductor is the rising overcapacity from Chinese IDMs and Fabless companies. This has led to pricing pressure and market share loss. That will be a topic for another day. While automotive chips might have bottomed cyclically, it will be purely a trade given the structural headwinds they face from the Chinese.