2025 WFE outlook

China de-risked with TSMC and NAND as the main driver. Intel and Samsung are not coming back

As major memory and logic customers have reported their results, it is time to revisit the outlook for WFE (Wafer Fabrication Equipment) in 2025. We shall start from the equipment vendors

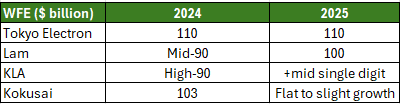

Source: Tokyo Electron, Lam Research, KLA, Kokusai

The WFE companies are not expecting a big increase in overall WFE spend in 2025. While Lam Research and KLA are looking at mid single digit growth in WFE, Tokyo Electron and Kokusai are looking at a flattish year. This is still slightly better than the expectation of a decline in WFE in 2025 due to weak memory outlook and capex cut at Samsung, Intel.

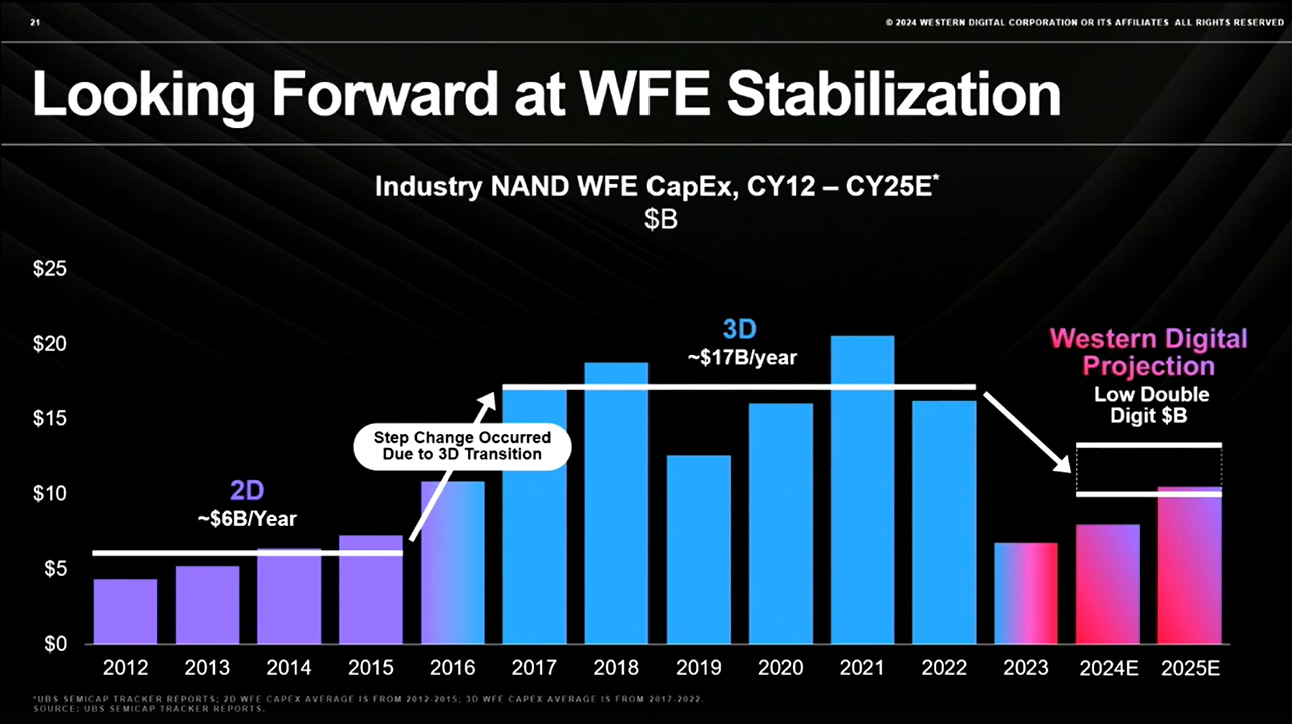

NAND > TSMC > DRAM > Logic

Source: Tokyo Electron, Lam Research, KLA, Kokusai

Contrary to what some might expect, NAND is actually the strongest growth driver for WFE in 2025. Tokyo Electron expects NAND capex to double while Kokusai is seeing a 25% increase. Both Lam Research and KLA are also seeing growth in NAND capex. On the other hand, outlook for both logic and DRAM are flattish.

In NAND, the industry is looking to transition the current installed capacity to higher layer counts to achieve better device performance at lower bit cost.

But at the same time, on the last call, I mentioned this point that about 2/3 of the bids are still being manufactured on nodes below 200 layers. And what happens as you move above 200 layers is not only do you have to upgrade the existing tools, but you have to start adding additional tools to deal with the complexity of that transition.

Source: Lam Research

NAND prices continue to decline and major producers are cutting production level, so no one is really expanding greenfield capacity. As NAND spending has been at a very subdued level for 2 years (down 50% from 2022 peak), memory makers are starting to upgrade their layer count again. We are definitely not in the new era of NAND that Western Digital was talking about where there is an end to the layer race.

Source: Western Digital - The New Era of NAND

Among the major NAND producers, it is likely to be Samsung, Hynix and YMTC that are driving the upgrade cycle. Samsung is upgrading its V6 NAND to V8 this year and will be developing 400L NAND in 2026. Hynix will be upgrading to 321L NAND this year, followed by 400L NAND in 2026. YMTC is working hard to achieve a breakthrough to 160L NAND with the help of AMEC in China. Lam Research is no longer able to supply etching tool to YMTC. While Kioxia will like to spend more, they are constrained financially and by their partner Western Digital.

Logic - TSMC is the kingmaker

Leading edge logic demand is strong as TSMC is looking at mid-20% growth in revenue for 2025. TSMC had guided for mid 30% in capital intensity last year so it was no surprise that it raised its capex from $ 29.8 billion in 2024 to $38 - 42 billion in 2025. With a 20% revenue CAGR from 2024 to 2029, TSMC will continue to spend more in capex on the leading edge. N2 is set to start mass production this year and ramp in volume in 2026. As the number of new tape-out for N2 in the first 2 years will be higher than both N3 and N5, N2 is a big volume ramp in 2026 and 2027. N2 is TSMC’s 1st GAA node, so this will disproportionately benefit ASMI and Lam Research which are the main ALD provider.

Most will have known that Samsung and Intel have cut their logic capex. Intel has further cut their gross capex in 2025 from $20-23 billion to $20 billion. This is a 20% capex cut in 2025 after a 20% capex cut in 2024. Intel Foundry is not getting any significant customer in the next 2 years. Nova Lake, which is the next generation client CPU after Panther Lake, will continue to have some tiles outsourced to TSMC. Granite Rapid has been delayed to 1H 2026, while Falcon Shore will no longer be sold externally.

For Samsung, next generation Galaxy S25 will be 100% Qualcomm chipset as they are not using their in-house Exynos. This is the 2nd time in recent year since S23 that Exynos is not used in Samsung’s flagship phones. As Samsung’s lead edge node is progressing far worse than Intel, it has been losing clients such as Qualcomm to TSMC. TSMC has effectively monopolised N3 and beyond node. I highly doubt Samsung can turnaround the foundry business unless it gave up on the leading edge. The big question for Samsung Foundry is what are they going to do with the Taylor fab. Equipment move-in for Taylor fab has been paused and the ramp has been delayed from 2024 to 2026. Because N4 yield is unsatisfactory, Samsung is betting instead on N2 ramp in 2026 to save them. Samsung had earlier announced that Taylor fab investment is $17 billion and total spending in Texas will run up to $40 billion. Chips Act grant was subsequently cut to $4.75 billion from $6.4 billion. Samsung is not going to get any large order for N2, so this could become a $17-40 billion asset that has to be written off eventually.

DRAM

DRAM price continues to decline with the ramp of CXMT output, while HBM demand remains very strong. With DDR4 oversupply, DRAM producers are shifting their product mix to DDR5 and HBM. Although DRAM price is expected to recover in 2H 2025, overall DRAM capex will be muted. Both Hynix and Micron are constrained in their ability to expand capacity meaningfully due to a lack of cleanroom space. Hynix has guided for limited incremental capex with the mix shifting more towards infrastructure for Yong-in fab in 2027. Hynix’s M15X equipment spend will be about $10 billion spread over 2025 and 2026. Micron is waiting for Idaho and New York fab to be ready in 20-27 and 2028. Samsung is guiding for flattish capex in 2025 with a reduction in foundry and increase in memory (more for NAND).

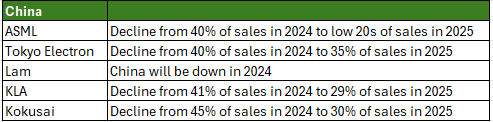

China

China was a hot topic for WFE manufacturers as it accounts for 40% of their revenue in 2024. With the export control and pull-forward demand (especially DUV) from China, it was inevitable that China revenue will decline. China is now going to be 30% of revenue for the WFE producers and likely be even lower in 2026. ASML’s China sales is a leading indicator for the other WFE’s China sales. Both KLA and Lam have seen a $500 million and $700 million impact from export control respectively.

Another angle that investors often miss is how fast the China WFE manufacturers are ramping up in capabilities. Because of export control, YMTC has to rely on local manufacturer such as AMEC for etching tool. The top 3 WFE manufacturers in China (Naura, AMEC and ACM Research) have grown their revenue by more than 30% to USD 6 billion. Naura expects local WFE companies to grow their revenue from USD 8.2 billion in 2024 to USD 11 billion in 2025 (11% global market share). The 33% growth is very impressive, considering China WFE will be down 15-20% in 2025. Domestic import substitution rate for WFE will be 35% in 2025.

China WFE demand is expected to decline as CXMT is slowing down their capex in 2025 while mature logic is suffering from overcapacity. On the other hand, YMTC is expected to ramp up its 160L investment after being crippled temporarily by the export control.

Share Shift

Tokyo Electron has secured mass production POR for NAND channel hole etching with its cryogenic etching for 2026. Given Tokyo Electron’s market share of 10-15% in 3D NAND etching, this will be a market share gain opportunity from Lam Research. However, I do not expect Tokyo Electron to monopolise cryogenic etching as Lam Research has come out with similar product.

Lam Research has secured POR for dry resist for DRAM, which will take away some market share from Tokyo Electron.

ASML - Peak lithography until High-NA arrives in 2030

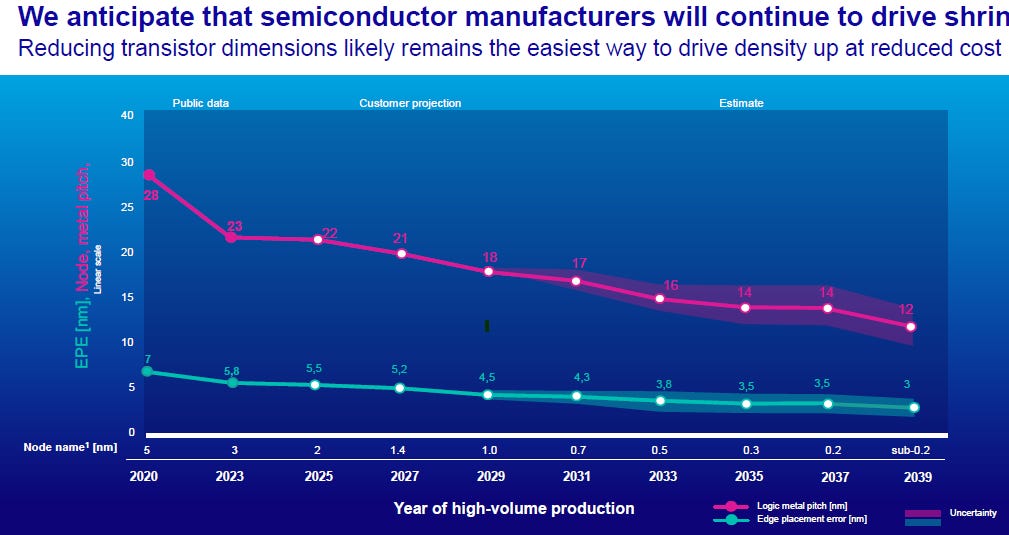

The bigger share shift opportunity remains the shift towards materials engineering from lithography scaling for the rest of the decade. Deposition and etching will outperform as lithography intensity is reduced. Logic metal pitch will only shrink by 10% from 23nm in 2023 to 21nm in 2027 compared to the 20% shrink from 28nm in 2020 to 23nm in 2023. TSMC’s N2 node is reliant on the Gate-All-Around (GAA) architecture which will favor Atomic Layer Deposition (ALD) equipment and etching tool. ASMI is the biggest beneficiary of single-wafer ALD which will continue to grow in important into CFET and 3D DRAM. Lam Research is seeing its ALD revenue growing by at least 50% in 2025 from $1 billion in 2024. Lam Research will only benefit from the use of lateral etching in GAA.

Source: ASML Investor Day

Source: Lam Research

As TSMC moves towards A16 in 2026, backside power delivery will be the key driver. EV Group will be a big beneficiary as the main provider of wafer-to-wafer hybrid bonder. CMP tool (Applied Material and Ebara) and grinding tool (Disco) will also benefit from content growth.

ASML will outperform WFE again when High-NA EUV is adopted by TSMC near the end of the decade. 5 years is a long time and it remains to be seen if there will be further delay in adoption. 3D DRAM is also a threat to ASML in the longer term, although ASML don’t see it happening in 2030.

Conclusion

With China de-risked and the underperformance against SOXX, it might be time to relook at the WFE manufacturers again. Companies such as ASMI, Lam Research and KLA are clear WFE share gainers over the next few years. Tokyo Electron and Applied Material will benefit to a smaller extent, while ASML’s sales underperformance will be seen from 2026. China sales will continue to dwindle for foreign players as domestic substitution continues.

2026 should be a stronger year in capex spending as TSMC continues to increase capex to meet the demand of N2. Hynix and Micron will also start to pull in equipment in 2H 2026 for their new greenfield plants.

Wouldn't it make more sense to go long the top 3 WFE in China? As in Naura, AMEC, ACMR? Localization trends will continue regardless of total slowdown in China WFE spend within next 2 years.